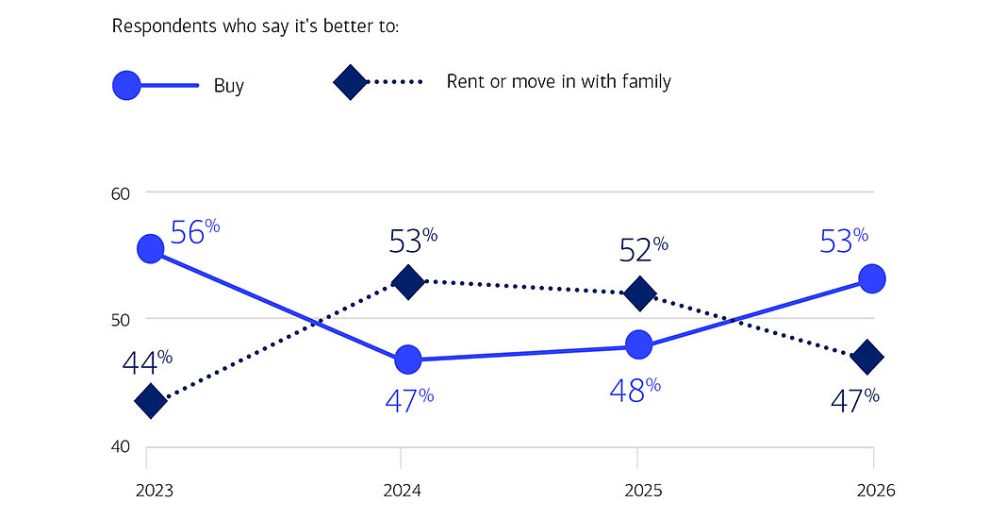

For the first time since 2023, a majority of consumers say it’s better to buy a home in the current market.

According to the latest Bank of America Homebuyer Insights Report, conducted in partnership with Bank of America Institute, 53 percent of respondents now favor buying over renting or moving in with family (47 percent).

The survey also revealed positive shifts in consumer sentiment toward homeownership, including:

- 90 percent of respondents say a home is a valuable investment, up from 79 percent in 2025.

- 94 percent say homeownership provides stability, up from 83 percent in 2025.

- 32 percent say they are more confident in their ability to buy a home this year, up from 27 percent last year.

“We are seeing meaningful changes in attitudes toward homeownership,” said Matt Vernon, head of consumer lending at Bank of America. “Despite real and persistent challenges in the market, buyers and owners are increasingly optimistic and many are starting to move forward rather than waiting on the sidelines.”

Insights point to movement in the market: Even as attitudes shift, prospective buyers increasingly cite affordability as the top barrier to homeownership, with 58 percent pointing to expensive home prices (vs. 46 percent in 2025) and 47 percent pointing to high interest rates (vs. 40 percent in 2025). Bank of America Institute’s latest On the Move analysis also shows rent payments are declining, suggesting renters are trading down by opting for smaller units, fewer amenities, more remote areas, or shared living arrangements to cut costs.

Still, intent to purchase a home is rising:

- Fewer prospective buyers are waiting for market conditions to improve before purchasing. In this latest survey, 71 percent said they expect prices and interest rates to fall and are waiting until then to buy a home, compared to 75 percent in 2025, with Gen Z (68 percent vs. 74 percent) and Millennials (70 percent vs. 77 percent) leading this shift.

- 52 percent of current homeowners say they expect to buy another home (a new or additional one) and more are accelerating their timelines, with 22 percent planning to buy within the next year, compared to 15 percent in 2025.

The lock-in effect, while still present, appears to be easing. The survey points to increased willingness to compromise, with more prospective homebuyers open to moving—even if it means paying a higher interest rate for:

- A more affordable area (76 percent vs. 71 percent in 2025 and 68 percent in 2024).

- Their dream home becoming available (75 percent vs. 69 percent in 2025 and 67 percent in 2024).

- A better location (71 percent vs. 65 percent in 2025 and 63 percent in 2024).

AI becomes part of the homebuying journey: One in five prospective buyers and current homeowners (20 percent) used AI tools or chatbots in the past year for homebuying research, including 28 percent of Millennials and 32% of Gen Z. Among those prospective buyers who used AI, top use cases include:

- Estimating affordability, mortgage payments, or closing costs (57 percent).

- General education and research about the process (55 percent).

- Researching neighborhoods, market trends, or property values (52 percent).

Although AI can be a useful tool, prospective buyers still prefer human expertise for key steps such as touring homes (55 percent) and legal or contractual advice (54 percent).

“AI is becoming a meaningful first step in the homebuying journey, especially for younger buyers. However, when it comes to high-stakes decisions, people still want trusted experts by their side,” said Vernon. “We find that clients prefer a mix of high-tech solutions such as Bank of America’s Digital Mortgage Experience–which streamlines the mortgage application process online or via mobile–paired with the high-touch experience and expertise of lending and real estate professionals along the way.”

Gen Z adapts to today’s market: Some Gen Z are taking on extra jobs (28 percent) or considering co-buying with friends or family (32 percent) to make homeownership more attainable and 31 percent plan to leverage homebuyer assistance programs, such as Bank of America’s Down Payment Grant, America’s Home Grant, or low down payment mortgages. By leveraging these resources, eligible homebuyers can receive up to $17,500 in combined down payment and closing cost assistance, or lock in a mortgage with a competitive rate and 3 percent down payment. Bank of America also offers free financial education tools, including Better Money Habits and Life Plan, to help buyers build confidence and plan for long-term financial goals.

Methodology: Sparks Research conducted a national online survey on behalf of Bank of America from April 13 to May 10, 2026. A total of 2,000 surveys (1000 homeowners / 1000 renters) were completed with adults 18 years old or older, who make or share in household financial decisions and who currently own a home/previously owned a home or plan to own a home in the future. Select questions allowed respondents to choose more than one answer, resulting in responses that may equate to more than 100 percent.